Table of Contents

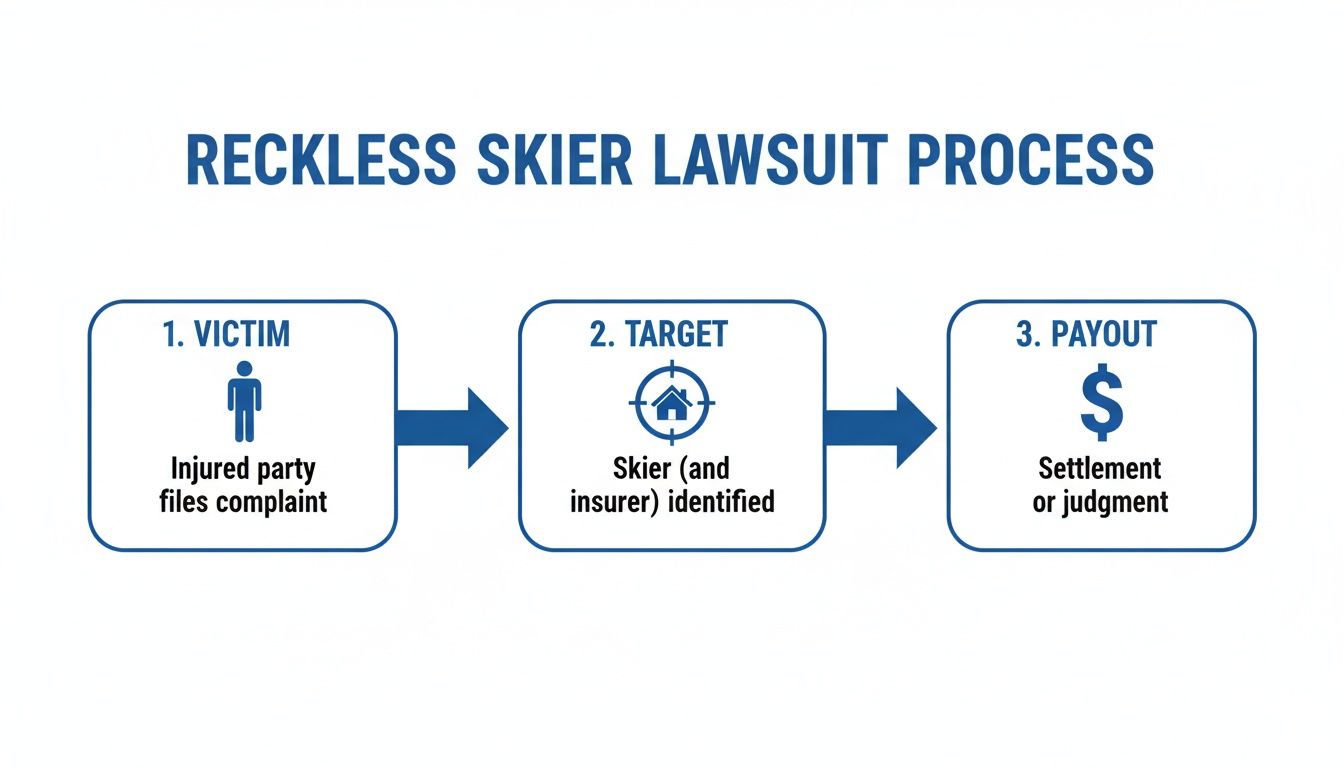

Yes — if another skier or snowboarder crashed into you and hurt you, you can file a personal injury claim against that person directly in Colorado. A collision caused by someone else's carelessness isn't just bad luck on the mountain. It's negligence, and the person responsible can be held accountable for the harm they caused.

This guide walks through how that claim actually works: who pays, what you have to prove, and the evidence you need to lock down before it disappears.

The Short Version

Here's the case in plain terms:

- You're suing the skier who hit you — not the resort, and not yourself.

- You're really reaching their insurance. Most of these claims are paid by the at-fault skier's homeowner's or renter's liability policy, not their personal savings.

- The resort waiver doesn't stop you. A waiver addresses the inherent risks of skiing — not another person's reckless conduct.

- Speed matters. The other skier is often a tourist who flies home in a day or two, and the evidence melts fast.

A Collision Isn't an "Inherent Risk" of Skiing

Insurance adjusters love to claim that getting hit on the mountain is just part of the sport — that you accepted the risk the moment you clicked into your bindings. Don't buy it.

There's a real difference here. Catching an edge on an icy patch and falling? That's an inherent risk of winter sports. Getting bulldozed from behind by someone skiing too fast and out of control? That's negligence. The person who hit you wasn't having an unlucky day — they failed to ski in a way that avoids the people in front of them.

Colorado's Ski Safety Act (C.R.S. § 33-44) governs how skiers and snowboarders are supposed to behave on the slopes, including the long-standing principle that the skier coming from uphill is in the better position to avoid a collision and bears the primary duty to do so. When someone violates that duty, it can support a negligence claim against them. For a deeper walkthrough of those on-slope duties, see our explainer on the Colorado Ski Safety Act.

What Reckless Skiing Usually Looks Like

The kinds of conduct that tend to put fault squarely on the other skier:

- Failing to avoid the skier downhill — the big one.

- Skiing too fast for the conditions or the crowd.

- Skiing beyond their ability and losing control.

- Not keeping a proper lookout — "I never saw you" isn't a defense; it's an admission.

- Ignoring posted signs or closures.

Who Actually Pays — It's Probably Not Their Savings Account

I hear this constantly: "Elliot, I don't want to ruin someone's life. Do I really have to sue another person?" It's a decent, human instinct. But it rests on a misunderstanding of how these claims work.

You're almost never going after the individual's bank account. You're going after their homeowner's or renter's liability insurance — and often an umbrella policy stacked on top of it.

"But he hit me on a mountain, not at his house. How does that cover this?" Because personal liability coverage tucked inside a standard homeowner's or renter's policy generally follows the policyholder away from home — including onto the slopes. So when an out-of-control skier from Texas or Florida collides with you at a Colorado resort, the claim can often reach their policy back home rather than their personal assets. Coverage always depends on the specific policy terms, so whether a given policy responds is something to confirm.

That reframes the whole thing. This isn't you versus some stranger. It's your claim against an insurance company that collected premiums for exactly this situation.

Finding Them — and Their Insurer — Is the Lawyer's Job

"The guy who hit me was gone before I got off the mountain. How do we even find him?" That's where having a lawyer earns its keep. The at-fault skier — usually a visitor — has every reason to disappear, and they're counting on the trail going cold. We don't let it.

The process is straightforward and aggressive:

- Secure the records. Demand the ski patrol report and any resort documentation right away.

- Locate the defendant. Use investigators to get a real name and address, even if they've left the state.

- Force disclosure. Once suit is filed, the defendant has to disclose their applicable insurance — they can't legally hide it.

- Put the insurer on notice. The fight moves to where it belongs: between your lawyer and their adjusters.

Your Evidence Has a Shelf Life Measured in Hours

The biggest threat to your case usually isn't the other skier's version of events. It's that the proof vanishes. Ski patrol reports get filed away, witnesses scatter to other states, and helmet-cam footage gets recorded over within days. The skier who hit you is probably on a plane home by the weekend, taking their name, address, and insurance info with them.

You can't be expected to chase all of this down while you're hurt and in shock — that's the lawyer's job. But knowing what matters helps. The three pieces of evidence to protect immediately:

- The ski patrol report. The first official record — names, a description of the collision, and initial injury notes.

- Witness contact info. Independent witnesses are gold; they dismantle the classic "you cut me off" defense. Get names and numbers on the spot. Here's how to write a useful witness statement.

- Helmet camera or GoPro footage. Video doesn't lie. It shows speed, trajectory, and who had the right of way.

Common Questions

How long do I have to file a reckless skier claim in Colorado?

There's a legal filing deadline (a statute of limitations) for personal injury claims, and missing it can permanently bar your case. For ski-collision injuries governed by the Colorado Ski Safety Act, that deadline is generally two years (C.R.S. § 33-44-111) — shorter than the deadline for many other injury claims. Practically, though, your real deadline is now — the evidence and witnesses disappear long before any legal deadline runs.

What if I was partly at fault?

Being partly at fault doesn't automatically end your case in Colorado, but how fault is divided can affect what you recover. This is also a classic insurance tactic — pin some blame on you to shrink the payout. Don't accept their framing. The duty of the uphill skier to avoid the person below is often central to sorting out who's actually responsible.

Should I take a cash offer from the other skier at the scene?

No. A few hundred dollars handed over "for the trouble" is someone trying to buy out of liability before you know how badly you're hurt. That sore knee today can turn into a torn ACL and surgery next week. Once you take the cash and they think you've waived your rights, your options narrow fast. Don't sign anything or accept money without understanding the full extent of your injuries.

Does my resort waiver stop me from suing another skier?

No. The waiver you signed is a contract between you and the resort about the inherent risks of skiing. It says nothing about another guest's reckless conduct and offers that skier zero protection. Assumption-of-risk covers the natural hazards of the sport — not someone who plows into you out of control.

Disclaimer: This post is for general information only and is not legal advice. Past results don't guarantee future outcomes, and reading this doesn't create an attorney-client relationship.

Talk to Conduit Law

You've got questions; we've got answers — and the consultation is free. If a reckless skier hurt you on a Colorado slope, call Conduit Law at (720) 432-7032. We'll review what happened, explain your options, and handle the fight with the insurance company from there.

For the bigger picture on skier, snowboarder, resort, lift, and waiver issues, see our Denver skiing accident attorney overview.

Written by

Elliot Singer, Esq.

Personal injury attorney at Conduit Law, dedicated to helping Colorado accident victims get the compensation they deserve.

Learn more about our team