Table of Contents

The insurance adjuster has a script. A neat little story where the villain isn't their client who was driving too fast on bald tires—it's the weather. They'll call the crash an "Act of God" and tell drivers everyone shares the blame when the roads get slick. This narrative conveniently shifts responsibility away from negligent driving behaviors. Colorado saw 628 traffic fatalities in 2023, many involving preventable circumstances like worn tire treads and excessive speed. Yet insurers routinely use weather as a shield, despite Colorado law requiring minimum liability coverage of $25,000 per person and $50,000 per accident under C.R.S. § 10-4-609. These limits exist precisely because accidents happen—and someone must bear financial responsibility. What's often overlooked: drivers remain accountable for maintaining safe vehicles and adjusting speed regardless of conditions. An adjuster's script doesn't change the legal standard. Colorado courts recognize that "Act of God" defenses fail when negligent driving contributed to the collision. Understanding this distinction matters when settlement negotiations begin.

For Denver-area winter crashes, our Denver car accident lawyers can evaluate whether speed, following distance, tires, visibility, or road conditions changed the fault analysis.

Let's get one thing straight, right now: Icy roads are not a legal excuse for reckless driving.

This isn't just a turn of phrase. It's the entire foundation of your case. As an icy road car accident attorney in Colorado, the job is to dismantle their convenient fiction with cold, hard, inconvenient facts. Negligence isn't excused by freezing temperatures—it's exposed by it. Colorado recorded 628 traffic fatalities in 2023, and winter conditions remain a persistent factor in serious collisions across the state. When drivers fail to adjust their speed, maintain proper following distance, or exercise reasonable care on icy surfaces, they've violated their legal duty. Under C.R.S. § 10-4-609, Colorado's minimum liability requirements demand $25,000 per person coverage. Yet 16% of Colorado drivers remain uninsured, leaving victims vulnerable. Winter weather doesn't create a liability shield; it clarifies responsibility. Defendants often argue conditions were "unavoidable," but Colorado law requires drivers to operate safely given existing conditions. That distinction—between excusing negligence and exposing it—determines whether victims receive the compensation they deserve.

The “Unavoidable Accident” Is the Oldest Lie in the Book

You saw it before they did. That weird, dark shimmer on the asphalt—the tell-tale sign of black ice on an otherwise clear day. You did what any responsible Colorado driver does: you eased off the gas, kept the wheel steady, and gave yourself space. You followed the rules. You were careful. Yet somehow, you still skidded. Still collided. Still ended up injured and wondering how this happened when you did everything right. This is where the "unavoidable accident" narrative kicks in—the oldest defense in the insurance playbook. But Colorado law disagrees. Under C.R.S. § 10-4-609, drivers are required to maintain minimum liability coverage of $25,000 per person. More importantly, drivers have a legal duty to operate vehicles safely under all conditions, including ice and poor weather. In 2023, Colorado recorded 628 traffic fatalities, many involving drivers who claimed conditions were simply beyond their control. That excuse rarely holds up in court—especially when negligence can be proven.

The driver behind you, however, was in a different world—a world where physics apparently takes a snow day. They were tailgating, probably texting, and definitely not paying attention to the road ahead. This reckless behavior is far from uncommon on Colorado roads. In 2023 alone, CDOT recorded 628 traffic fatalities, many stemming from preventable distracted and inattentive driving. Compound this with the fact that 16% of Colorado drivers operate uninsured vehicles, and the collision transforms from a mere fender-bender into a potential financial nightmare. Colorado law requires minimum liability coverage of $25,000 per person and $50,000 per accident under C.R.S. § 10-4-609, yet that may prove insufficient for serious injuries. When negligent drivers claim their accident was unavoidable, insurance companies often accept this narrative uncritically. The evidence—dashcam footage, phone records, skid marks, and witness testimony—frequently tells a different story, one of deliberate inattention and calculated risk that puts lives at stake.

When you slowed, their sedan went into a clumsy pirouette and slammed into your rear bumper. The first words out of their mouth weren't "Are you okay?" They were, "The ice! I couldn't stop. It was unavoidable." This excuse is as old as winter driving itself. Colorado's roadways saw 628 traffic fatalities in 2023, according to the Colorado Department of Transportation, yet weather-related claims dominate accident conversations. Drivers routinely invoke road conditions to deflect responsibility, even when their speed, following distance, or vehicle maintenance contributed directly to the collision. Under C.R.S. § 10-4-609, Colorado's minimum liability insurance requirements are $25,000 per person and $50,000 per accident—coverage that inadequately addresses serious injuries. Complicating matters further, approximately 16% of Colorado drivers operate uninsured vehicles. When someone invokes "unavoidable" conditions, it's worth examining whether their driving choices actually matched those conditions.

This is a lie. A tired, predictable, self-serving lie. It's the go-to excuse for every driver who thinks a Colorado winter is just a suggestion—and it's the first page in the insurance adjuster's playbook. They want the injured party to believe this was a random act of nature, a blameless event beyond anyone's control. But Colorado's roads claimed 628 lives in 2023, and the vast majority of those collisions involved preventable human choices: excessive speed, insufficient following distance, or failure to adjust driving conditions. Under Colorado Revised Statutes § 10-4-609, drivers are required to maintain minimum liability coverage of $25,000 per person and $50,000 per accident—a legal baseline that assumes drivers bear responsibility for safe operation. When adjusters invoke the "unavoidable accident" defense, they're attempting to shield negligent drivers from accountability. The reality is unforgiving: most winter accidents result from driver decisions, not meteorological inevitability.

It wasn't. It was a choice. Their choice.

Your Case Is Won by Proving Their Negligence Was the Real Hazard

The other driver already has their story straight. The ice came out of nowhere, they'll tell their insurer. I did my best, there was nothing anyone could do. But that narrative doesn't hold up under scrutiny. Colorado law, specifically C.R.S. § 10-4-609, requires drivers to maintain minimum liability coverage of $25,000 per person and $50,000 per accident—a baseline that assumes drivers are accountable for their actions. Weather is never a free pass to negligence. Even when roads are icy, drivers must exercise reasonable care: reducing speed, increasing following distance, and avoiding sudden maneuvers. With 628 traffic fatalities recorded across Colorado in 2023, courts and juries understand that driver behavior—not conditions alone—determines liability. To win a case, proving negligence means demonstrating that the other driver failed to adjust their conduct to match road hazards. Their insurance company knows this too, which is why their prepared statement requires careful examination by someone who understands Colorado accident law.

It's a convenient story that erases all responsibility. And it's almost never true. When negligence claims arise after a Colorado car accident, defendants and their insurers often retreat into narratives of unavoidable circumstance—bad luck, mechanical failure, or acts of God. These stories sound plausible until confronted with objective evidence. The stakes are real. Colorado recorded 628 traffic fatalities in 2023, underscoring how dangerous negligent driving truly is. Additionally, 16% of Colorado drivers carry no insurance, leaving injured parties vulnerable when accountability matters most. Proving negligence requires dismantling these convenient narratives with cold, hard facts: witness statements, accident reconstruction, maintenance records, and expert analysis. Under Colorado Revised Statutes § 10-4-609, minimum liability coverage stands at $25,000 per person and $50,000 per accident—a baseline that often proves insufficient for serious injuries. The goal is straightforward: establish that the defendant's breach of duty—not circumstance—caused the collision and resulting harm. Evidence, not excuses, determines liability and recovery.

Proving negligence in a winter crash means showing the other driver breached their duty of care—the non-negotiable legal obligation every driver has to operate their vehicle reasonably and prudently for current conditions. When another driver blames ice or snow, they're essentially confessing they failed to meet that standard. Colorado law requires all drivers to maintain minimum liability coverage of $25,000 per person and $50,000 per accident, according to C.R.S. § 10-4-609. Yet 16% of Colorado drivers remain uninsured, creating additional complications for accident victims. With 628 traffic fatalities recorded in Colorado during 2023, winter conditions demand heightened vigilance and adjusted driving behavior. A driver who slides on ice while traveling at unsafe speeds, following too closely, or using bald tires hasn't been victimized by weather—they've violated their duty of care. The negligence lies in failing to adapt to conditions, not in the conditions themselves. This distinction becomes critical when building a strong personal injury case.

Your Secret Weapon: Their Bad Tires

A driver who gets behind the wheel with bald tires on a snowy day is no different than one who drives drunk. They are knowingly operating a dangerous machine without the equipment to control it. That's a willful act of negligence—and it's incredibly powerful evidence in a personal injury claim. Colorado recorded 628 traffic fatalities in 2023, many of which involved preventable equipment failures. Tires are the only point of contact between a vehicle and the road, yet countless drivers ignore their deteriorating condition. When someone operates a vehicle with worn tires in hazardous weather, they're deliberately choosing speed over safety. Under Colorado law (C.R.S. § 10-4-609), drivers must carry minimum liability insurance of $25,000 per person and $50,000 per accident. Yet evidence of bald tires reveals something more damaging: conscious disregard for public safety. This negligence transforms a simple accident into a case where punitive damages may apply, signaling to juries that the defendant's conduct was reckless and inexcusable.

We aggressively investigate the condition of their vehicle:

- Tire Tread Analysis: We get the tread depth measured. If it’s below the legal minimum/obviously inadequate for winter conditions, their “unavoidable accident” defense evaporates.

- Maintenance Records: We subpoena service records. Did they ignore a mechanic’s recommendation to get new tires?

- Chain Law Violations: Did the crash happen on a stretch of I-70 where the Colorado Traction Law was active? Failing to use chains/proper tires is negligence, full stop.

The Truth Is in the Weather Data

The surprise of black ice is rarely a legitimate surprise. Weather forecasts, roadside temperature displays, and visible ice on overpasses are all clear warnings that responsible drivers should heed. Forensic weather reports from the National Weather Service provide critical evidence proving exactly what the conditions were at the precise time and location of a crash. This documentation becomes essential in Colorado, where 628 traffic fatalities occurred in 2023 according to the Colorado Department of Transportation. When negligent drivers ignore weather warnings and cause accidents, victims may pursue claims under Colorado's minimum liability insurance requirements of $25,000 per person and $50,000 per accident, as established by C.R.S. § 10-4-609. However, complications arise when uninsured drivers are involved—approximately 16% of Colorado motorists lack proper coverage. By analyzing National Weather Service data alongside accident circumstances, attorneys can establish whether drivers failed to adjust their behavior for known hazardous conditions, strengthening cases for injured parties seeking fair compensation.

We pull CDOT camera footage and traffic alerts to reconstruct what happened. We paint a picture that any reasonable driver would have—and should have—been on high alert. Colorado's weather conditions demand constant vigilance; in 2023 alone, CDOT recorded 628 traffic fatalities, many weather-related. Their failure to heed obvious warnings on the road—reduced visibility, slick conditions, or posted alerts—constitutes negligence. That negligence is what caused the harm. Under Colorado law (C.R.S. § 10-4-609), drivers must carry minimum liability coverage of $25,000 per person and $50,000 per accident. Yet 16% of Colorado drivers remain uninsured, creating additional complications. The weather data tells the truth: drivers had notice of dangerous conditions and chose to proceed recklessly anyway. The camera footage, combined with meteorological records and CDOT alerts, builds an undeniable narrative. Reasonable drivers adjust their behavior in adverse conditions. Those who don't bear responsibility for the consequences.

We Know How to Dissect Colorado’s Worst Winter Crashes

The insurance adjuster wants to lump every winter collision into a single, blameless category called bad weather. But the chaos on I-25 during the first snow is a whole different beast from a black ice spinout on a mountain pass. Colorado recorded 628 traffic fatalities in 2023, yet many of these crashes involve negligence that weather cannot excuse. Each scenario demands distinct analysis: visibility conditions, road treatment history, vehicle maintenance, and driver behavior all factor differently depending on the specific circumstances. Black ice accidents differ fundamentally from snow-packed highway pile-ups, which differ again from weather-related accidents caused by reckless driving. Insurance companies routinely exploit this ambiguity, grouping cases together to minimize payouts. Understanding Colorado's minimum liability requirements under C.R.S. § 10-4-609—$25,000 per person and $50,000 per accident—becomes critical when fighting inadequate settlement offers. These winter crash scenarios are tragically predictable, and each deserves meticulous investigation to separate genuine weather causation from driver negligence and insurance company tactics designed to undervalue legitimate claims.

Scenario A: The Rear-End Collision on Ice

This is the classic rear-end collision scenario. A driver does everything right—maintaining safe speed, following traffic conditions, driving defensively. Then, BAM. The driver behind suddenly slams into the trunk, and the at-fault driver immediately blames the ice. While winter weather certainly creates hazardous driving conditions across Colorado, it does not absolve a driver of their legal duty to maintain safe control of their vehicle. Colorado law requires all drivers to carry minimum liability insurance of $25,000 per person and $50,000 per accident, as outlined in C.R.S. § 10-4-609. Unfortunately, 16% of Colorado drivers remain uninsured, complicating recovery efforts. With Colorado recording 628 traffic fatalities in 2023 alone, rear-end collisions demand serious attention. Whether ice played a role or not, the trailing driver bears responsibility for maintaining adequate stopping distance and speed control relative to road conditions.

This is a confession, not a defense. It's a direct admission they were following too closely for the conditions. Colorado law is crystal clear: every driver must maintain a safe following distance, which expands dramatically on ice. The standard three-second rule becomes an eight- to ten-second necessity. When a driver ignores this requirement, they're violating C.R.S. § 10-4-609, which establishes mandatory liability insurance minimums of $25,000 per person and $50,000 per accident. This matters because Colorado recorded 628 traffic fatalities in 2023, with rear-end collisions representing a significant portion of preventable crashes. Additionally, approximately 16% of Colorado drivers operate uninsured, leaving victims without financial recourse. Following too closely in winter conditions isn't merely careless—it's negligence per se, meaning the breach of the safety statute itself proves fault. Insurance companies understand this distinction immediately. When weather compounds the violation, liability becomes nearly impossible to dispute, making these cases among the strongest in personal injury law.

Scenario B: The Loss-of-Control Spinout

A car in the next lane loses traction, spins, and careens into the vehicle beside it. In these chaotic moments, the other driver will often claim they were helpless—that road conditions, mechanical failure, or sudden circumstances left them with no ability to prevent the collision. However, Colorado law recognizes that drivers have a duty to maintain control of their vehicles under all conditions. According to Colorado Department of Transportation data, 628 traffic fatalities occurred in Colorado during 2023, with loss-of-control accidents representing a significant portion of these preventable tragedies. When investigating spinout claims, insurers and courts examine whether the driver exercised reasonable care, maintained appropriate speed, and kept their vehicle in safe operating condition. Additionally, 16% of Colorado drivers carry no insurance, complicating recovery efforts. Under C.R.S. § 10-4-609, minimum liability coverage is $25,000 per person and $50,000 per accident—often insufficient for serious injuries resulting from negligent loss of control.

This points directly to negligence. Vehicles don't just spontaneously lose control. They lose control because they are moving too fast for the conditions. The spinout itself is powerful evidence of excessive speed. Colorado law recognizes this principle through liability standards codified in C.R.S. § 10-4-609, which establishes minimum liability coverage of $25,000 per person and $50,000 per accident. When a driver loses control, investigators examine whether speed exceeded safe limits for weather, road surface, and visibility. This analysis becomes critical given Colorado's traffic safety landscape: the state recorded 628 traffic fatalities in 2023 alone, with speed and loss of control contributing to many preventable crashes. Additionally, uninsured or underinsured drivers complicate recovery efforts—approximately 16% of Colorado drivers operate without proper insurance. The spinout demonstrates that the at-fault driver failed to adjust speed appropriately, establishing the negligence necessary to pursue a claim for damages and hold them accountable for injuries and losses resulting from their reckless operation.

Scenario C: The I-70/I-25 Multi-Car Pileup

These chain-reaction wrecks that shut down I-70 or I-25 feel impossibly chaotic. But figuring out fault isn't impossible—it’s just complicated.

The process involves meticulously reconstructing the sequence of events to find the first negligent act that set off the chain reaction. Was it a trucker going too fast for the grade? A driver on bald tires who spun out? Perhaps an uninsured motorist weaving between lanes without proper coverage—a concern given that 16% of Colorado drivers lack insurance, according to the Insurance Research Council. Determining which driver initiated the cascade is critical for liability purposes. Under Colorado law (C.R.S. § 10-4-609), minimum liability coverage requires $25,000 per person and $50,000 per accident, yet these limits often prove insufficient in multi-car pileups. Colorado recorded 628 traffic fatalities in 2023, many involving multi-vehicle collisions on congested interstate corridors. Identifying the initial negligent act establishes which party bears primary responsibility and whose insurance coverage must respond first. This foundational determination shapes the entire claim and recovery strategy.

Investigating these pileups requires an icy road car accident attorney in Colorado with the resources to immediately secure all police reports, interview dozens of witnesses, and hire accident reconstruction experts to analyze the physics of each impact. Colorado recorded 628 traffic fatalities in 2023, underscoring the devastating potential of multi-vehicle collisions. The investigation must account for multiple liable parties, each carrying minimum liability coverage of $25,000/$50,000 under C.R.S. § 10-4-609—though this statutory minimum often proves insufficient for serious injuries. Complicating matters further, approximately 16% of Colorado drivers are uninsured, meaning some responsible parties may lack any coverage whatsoever. The insurance company's dream is chaos; our job is to find the clarity that gets victims paid. Thorough investigation identifies every contributing factor, preserves crucial evidence, and builds the compelling case necessary to hold negligent drivers accountable and secure maximum compensation.

The Playbook Insurance Companies Use to Cheat You

Right after the crash, the other driver's insurance adjuster will call. They will sound impossibly calm and reasonable, speaking as though they're simply trying to help. Don't be fooled. Every word is part of a carefully crafted script designed to save their company money by taking it from the injured party. In Colorado, where traffic fatalities reached 628 in 2023 alone, these interactions matter enormously. The adjuster knows the state's minimum liability requirements—$25,000 per person and $50,000 per accident under C.R.S. § 10-4-609—and they know how to keep settlements well below those limits. They'll ask leading questions, request unnecessary documentation, and build a paper trail that serves their interests, not the claimant's. With 16% of Colorado drivers uninsured, the pressure to settle quickly is even greater. Understanding this playbook is essential. Insurance adjusters aren't advocates for accident victims; they're trained to minimize payouts and protect corporate profit margins.

Their entire strategy is built on one dishonest idea: that the ice makes everything confusing and, ultimately, a shared problem. They want victims to feel uncertain and grateful for whatever they offer. This tactic is especially effective in Colorado, where winter conditions contribute to serious accidents—the state recorded 628 traffic fatalities in 2023 alone. Insurance adjusters exploit this uncertainty by suggesting that weather-related collisions are somehow less clear-cut, making liability harder to establish. They'll imply that both parties share responsibility, even when the evidence suggests otherwise. Under Colorado law (C.R.S. § 10-4-609), drivers must maintain minimum liability coverage of $25,000 per person and $50,000 per accident. Yet with 16% of Colorado drivers uninsured, many victims already feel vulnerable. Insurance companies weaponize this vulnerability, counting on injured parties to accept lowball settlements rather than fight for fair compensation. Understanding this playbook is the first step toward protecting yourself.

They will tell you everyone is at fault because of the ice.

This line is their ace in the hole. They use it to justify a ridiculously low offer, claiming that since everyone was sliding, everyone shares a piece of the blame. It's a cynical distortion of how the law actually works. Negligence isn't erased by freezing temperatures; it's magnified by them. Colorado law, codified under C.R.S. § 10-4-609, establishes minimum liability coverage of $25,000 per person and $50,000 per accident—requirements that exist precisely because dangerous driving causes serious injuries. Winter conditions don't eliminate responsibility; they increase the duty to drive safely. When drivers fail to adjust speed, maintain proper following distance, or use appropriate tires, they've violated that heightened duty. Colorado recorded 628 traffic fatalities in 2023, many occurring in adverse weather. Insurance adjusters know this. Yet they weaponize icy roads as a defense strategy, suggesting shared fault where none exists. This approach systematically underpays legitimate claims and leaves injured drivers with inadequate recovery.

Then, they'll downplay your injuries and rush you to settle. Insurance adjusters want your signature before you've seen a doctor, before you understand the true cost of your medical bills, and certainly before you've called a lawyer. This strategy is particularly aggressive in Colorado, where 16% of drivers remain uninsured, and minimum liability coverage is only $25,000/$50,000 under C.R.S. § 10-4-609. Given that Colorado recorded 628 traffic fatalities in 2023 alone, serious injuries happen frequently—yet insurers still pressure victims into accepting lowball offers. They know that once you sign a release, the claim is closed. They're counting on confusion and financial desperation to prevent victims from discovering the full extent of their damages, from lost wages to long-term medical care. The insurer's goal isn't fairness; it's minimizing their payout before the injured party fully grasps what they've actually lost.

They will tell you everyone is at fault because of the ice. Don't believe them.

The adjuster's first offer is never their best offer. It is the lowest number they think an injured driver might be desperate or uninformed enough to accept. This is a calculated strategy, not a genuine settlement proposal. Recognizing this game is the first step to beating it. Insurance companies know that many Colorado drivers are vulnerable. With 16% of Colorado drivers uninsured and minimum liability coverage of just $25,000 per person under C.R.S. § 10-4-609, many accident victims face serious financial pressure. When combined with the reality that Colorado recorded 628 traffic fatalities in 2023, the stakes of underpayment become clear—families cannot afford to accept less than what their injuries are truly worth. Adjusters rely on claimants accepting lowball offers out of fear, pain, or simple lack of knowledge about claim valuation. Understanding that their opening bid is intentionally insufficient empowers injured parties to negotiate confidently and pursue fair compensation.

Your Job at the Scene: Preserve the Melting Evidence

The moments after a crash are chaos. Adrenaline is pumping. Witnesses are scattered. But in this chaos, critical evidence is literally melting away—skid marks fade, vehicle positions shift, and memories become unreliable. In Colorado, where 628 traffic fatalities occurred in 2023, the decisions made in those first minutes after impact can determine the outcome of an entire case. Adding complexity, approximately 16% of Colorado drivers carry no insurance, making thorough documentation even more vital. Under C.R.S. § 10-4-609, minimum liability coverage is $25,000 per person and $50,000 per accident, yet underinsured motorists remain common. Photographs of vehicle damage, road conditions, and debris patterns; written accounts from witnesses; and detailed descriptions of the scene preserve evidence before it disappears. What happens next—how the scene is documented and protected—can make or break a case. The window to capture this evidence is narrow and unforgiving.

- Rule #1: Take Pictures of Their Tires. I cannot overstate this. Get close-up, clear photos of the tread on all four of the other driver's tires. A photo of bald tires on a snowy day can single-handedly dismantle their "unavoidable accident" defense.

- Document Everything. Take wide shots showing the final resting positions of all vehicles and the road conditions. Capture photos of the specific patch of ice they’re blaming. Get detailed pictures of the damage to both vehicles.

- Get Witness Info. A neutral third party who saw the other driver speeding or tailgating is an invaluable asset. Get their name and number.

- Get Medical Attention. Even if you feel fine, adrenaline can mask serious injuries like whiplash or a concussion. A medical record from the day of the crash creates a direct link between the collision and your injuries.

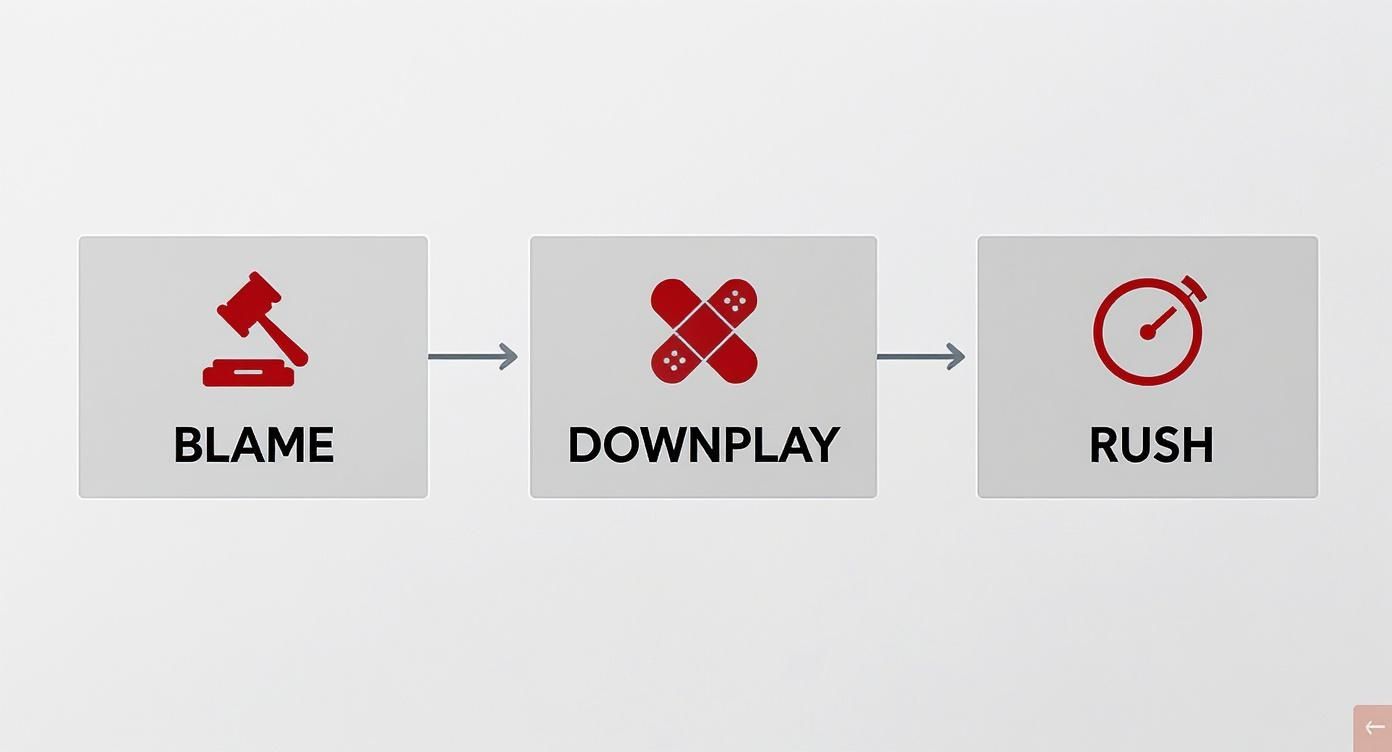

The insurance company has a predictable three-step playbook they almost always follow, as you can see below.

This process—blame the conditions, downplay your injuries, and rush into a quick, lowball settlement—is designed to protect their profits, not the injured party. Insurance adjusters know that Colorado's minimum liability requirements (C.R.S. § 10-4-609) set a floor of $25,000/$50,000, but they'll fight to keep payouts well below what injuries truly warrant. Given that Colorado recorded 628 traffic fatalities in 2023 alone, the stakes of these collisions are undeniably high. When uninsured drivers enter the equation—affecting roughly 16% of Colorado motorists—the pressure to settle quickly intensifies further. Adjusters weaponize time, hoping victims accept insufficient compensation before evidence disappears, witnesses' memories fade, and documentation becomes harder to obtain. Understanding this calculated strategy helps accident victims recognize when settlement offers fall short of actual damages and when legal representation becomes essential to protecting long-term interests.

In Colorado, our roads present unique dangers that claim far too many lives. The I-70 corridor between Vail and Glenwood Springs saw over 300 crashes in 2024, many linked to black ice. Denver's I-25 experienced 1,200 crashes in the same period, often caused by distraction and slick conditions. These alarming statistics reflect a broader crisis—Colorado recorded 628 traffic fatalities in 2023 alone, according to CDOT data. Adding to the complexity, 16% of Colorado drivers carry no insurance, leaving injured parties vulnerable. Under Colorado law (C.R.S. § 10-4-609), minimum liability coverage is $25,000 per person and $50,000 per accident, yet many accident victims face significant uncompensated losses. These numbers demonstrate that what seems like an accident is often part of a predictable—and preventable—pattern. Understanding these risks underscores why proper documentation and evidence preservation at the accident scene becomes crucial to protecting your legal rights and recovery options.

Disclaimer: This blog post is for informational purposes only and does not constitute legal advice. The information provided does not create an attorney-client relationship. Past results do not guarantee future outcomes.

At Conduit Law, we cut through the noise. The insurance company has a script—we have a strategy built on facts. If you were hurt because another driver refused to respect a Colorado winter, let’s talk. I got you. Call us for a free, no-obligation case evaluation.

Written by

Elliot Singer, Esq.

Personal injury attorney at Conduit Law, dedicated to helping Colorado accident victims get the compensation they deserve.

Learn more about our team