Table of Contents

If you were hurt in a Colorado accident and worry that you were partly to blame, here's the short answer: you can still recover money — as long as you were not more than 50% at fault. Colorado uses a rule called modified comparative negligence. Your share of the blame reduces your payout dollar for dollar, and if your fault crosses 51%, you recover nothing. That single percentage point is where the whole fight happens.

Below, we break down exactly what the rule means for your recovery, show the math with real numbers, and explain why insurance adjusters spend so much energy trying to pin a few extra points of fault on you.

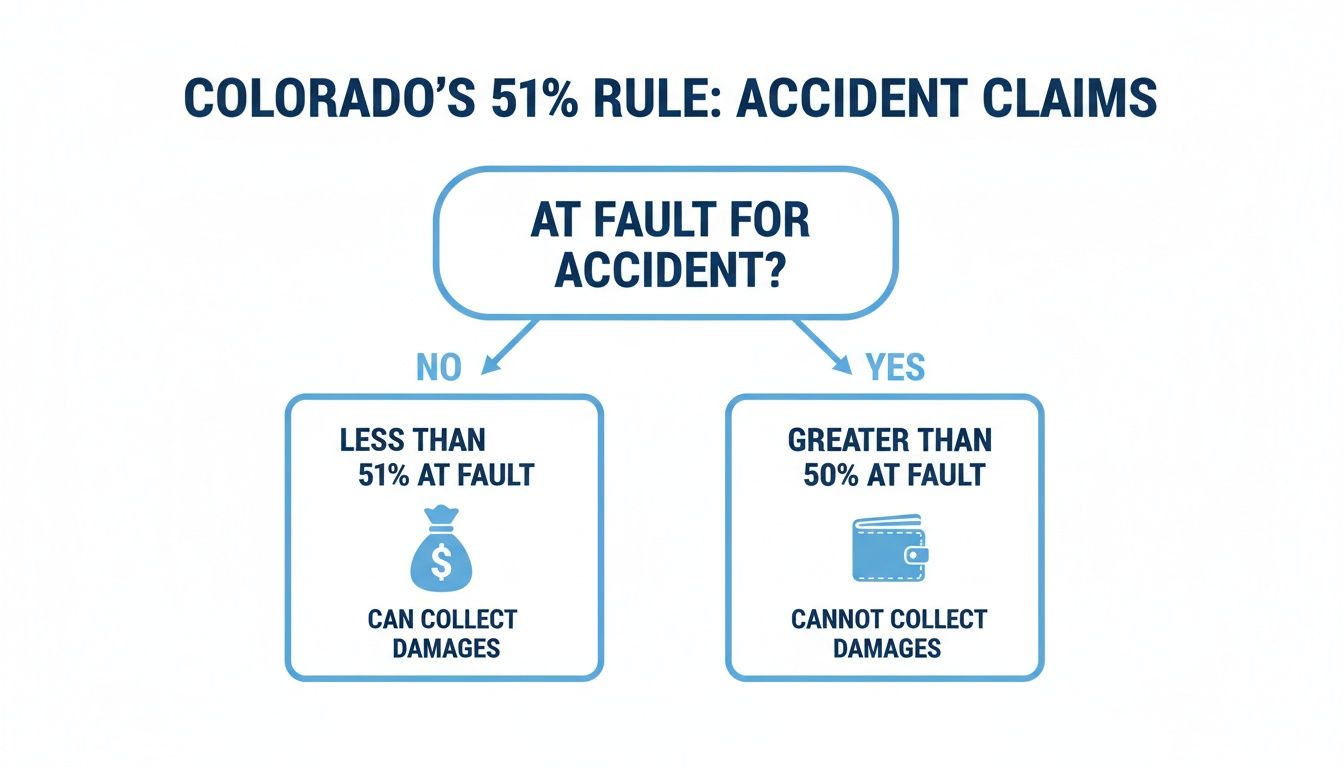

What Colorado's 50% Rule Actually Means

Colorado follows a "modified comparative negligence" standard. In plain English: a jury assigns each party a percentage of fault for the accident, and your compensation is reduced by your share. You can recover as long as your fault is 50% or less. The moment it hits 51% — majority fault — your claim is barred entirely and you get nothing.

That hard line is what lawyers call the "51% cliff." At 50% fault you still walk away with half your damages. At 51% you walk away with zero. Not everywhere works this way — some states let you recover even when you're 99% at fault — but Colorado doesn't, and that makes every percentage point worth fighting over.

This rule lives in Colorado's modified comparative negligence statute, C.R.S. § 13-21-111. The statute lets an injured person recover only if their own fault is less than the fault of the party they're seeking to recover from; the award is then reduced by the injured person's percentage of fault, and recovery is barred once that share reaches 50 percent or more.

How the Math Works: Fault Percentage to Recovery

The mechanics are simple once you see them. Take your total damages, then subtract your percentage of fault. Here's what that looks like on a $100,000 claim:

| Your Percentage of Fault | Can You Recover? | Your Payout on a $100,000 Claim |

|---|---|---|

| 0% | Yes | $100,000 |

| 30% | Yes | $70,000 (reduced by your 30%) |

| 50% | Yes | $50,000 (reduced by your 50%) |

| 51% | No | $0 (claim completely barred) |

The difference between 50% and 51% is the difference between a fair recovery and a total loss. That's not an accident in the way the law is written — it's a hard, all-or-nothing line, and it's exactly the line the insurance company will try to push you across.

Three Real-World Examples

The Aurora Fender-Bender

You get T-boned by someone who ran a stop sign. Total damages: $50,000. The adjuster finds out you were going five miles over the limit and assigns you 15% fault. Since 15% is well under 50%, you can still recover — but your award drops.

- The math: $50,000 − 15% ($7,500) = $42,500.

- The takeaway: Your "minor" infraction just cost you $7,500.

The Fort Collins Slip and Fall

You slip on an unmarked wet floor in a grocery store and rack up $100,000 in damages, including pain and suffering. The store's insurer pulls the security footage, sees you glancing at your phone, and assigns you 30% fault. Still under 50%, so you recover — minus your share.

- The math: $100,000 − 30% ($30,000) = $70,000.

- The takeaway: A moment of distraction — something every human does — is being used to dock you $30,000. For more on valuing those losses, see our guide on how to calculate pain and suffering damages.

The I-70 Pileup

A truck, another car, and you are all caught in a serious collision. Damages total $500,000 in medical bills, lost wages, and pain and suffering. A jury decides the truck driver was 60% at fault, the other car 20%, and you 20% for following too closely. Your 20% is below the bar, so you recover.

- The math: $500,000 − 20% ($100,000) = $400,000.

- The takeaway: That 20% sliver of blame vaporized a six-figure chunk of your recovery. This is why we fight over every single percentage point.

Why Insurance Adjusters Care So Much About Your Fault

Now you can see why the adjuster sounds so friendly on that first call — and why, a few minutes in, they start asking about what you could have done differently. Every percentage point of fault they shift onto you is money saved for their company. Even if their driver was 99% wrong, they'll dig for the 1% they can hang on you, because doing so does two things:

- It reduces your payout, dollar for dollar.

- If they can push you past 50%, it kills your claim entirely.

Here are the moves to watch for.

The recorded statement ambush

The adjuster calls and asks for a "quick recorded statement to process the claim." It isn't a chat — it's an interview built to get you on tape. A polite "I'm so sorry this happened" gets twisted into an admission. A hesitant "I guess I didn't see them until the last second" becomes proof of inattention. Don't give a recorded statement to the other side's insurer without talking to a lawyer first.

Misstating the law

Adjusters love to play legal scholar. They'll tell you that because you were changing lanes, turning left, or backing up, you're "automatically" partly at fault. That's not how it works — Colorado requires proof of actual negligence, not just that you were performing a normal driving maneuver. Don't accept a fault percentage just because someone on the phone said so with confidence.

Weaponizing your medical care

Couldn't get a doctor's appointment for two weeks? Missed a physical therapy session for a family emergency? The adjuster will argue any gap in treatment means you either weren't really hurt or made your injuries worse. They ignore the real reasons care gets delayed — cost, work, transportation — and frame the gap as your fault.

Blaming the victim

Sometimes the arguments are just desperate: your shoes in a slip-and-fall, your music being too loud in a crash. These are jabs thrown to see what sticks and to make you doubt yourself. The end game is always the same — inflate your fault enough to shrink or zero out the claim.

Build Your Evidence Before They Build Their Story

You can't stop the insurer from trying to shift blame, but solid evidence makes it much harder. In a fault dispute, the side with the better documentation usually wins. Your word against theirs is a toss-up; your word backed by objective proof is a knockout. Here's what to do after a crash:

- Photograph everything. Vehicle damage, skid marks, traffic signs, debris, weather. There's no such thing as too many photos.

- Get the police report. It isn't legally binding, but an officer's initial fault assessment can shut down an adjuster's argument before it starts.

- Collect witness info. Names and numbers of anyone who saw it. An independent witness can dismantle a blame-shifting story.

- Preserve evidence. Keep damaged property — clothing, helmet, phone. Don't repair your car until a lawyer says it's okay.

One more thing worth knowing: in Colorado you generally have three years from the date of a motor-vehicle injury to file a personal injury lawsuit (C.R.S. § 13-80-101(1)(n)), while many other negligence claims carry a shorter two-year deadline (C.R.S. § 13-80-102). The exact window depends on the type of claim, so confirm yours with an attorney. Waiting lets evidence fade and memories blur, so it pays to act early.

This can all feel overwhelming, and you don't have to handle it alone. The insurance company has a team working to minimize your claim — you deserve someone in your corner doing the opposite. If you want to understand where you actually stand on fault, call us for a free consultation at (720) 432-7032.

Disclaimer: This post is for informational purposes only and does not constitute legal advice. Reading it does not create an attorney-client relationship. Every case is unique — consult a qualified attorney about the specifics of your situation.

Written by

Elliot Singer, Esq.

Personal injury attorney at Conduit Law, dedicated to helping Colorado accident victims get the compensation they deserve.

Learn more about our team