Table of Contents

You did everything right. The snow squall moved in over the Front Range, and the decision was made not to drive. An app—Uber, Lyft, or another rideshare service—was tapped, placing safety in the hands of a professional driver. Yet even the most responsible choices can't always prevent accidents. If a rideshare driver's negligence caused injury, Colorado law provides important protections. Under Colorado's modified comparative negligence standard (C.R.S. § 13-21-111), an injured passenger can recover damages even if partially at fault, as long as the driver bears more than 50% responsibility. Non-economic damages—covering pain, suffering, and emotional distress—are capped at $1,500,000 as of 2025. Importantly, Colorado law provides a three-year statute of limitations (C.R.S. § 13-80-101) for filing personal injury claims. This deadline is critical; claims filed after three years are typically barred. Understanding these legal frameworks helps injured passengers navigate their options after a rideshare accident.

If a winter rideshare crash also involves another negligent driver, our Denver car accident attorneys can evaluate both the ordinary auto claim and the Uber/Lyft insurance layer.

Then came the jolt. The sickening crunch of metal on black ice.

One minute a passenger is in the back seat, heading to DIA or just crossing town. The next, the rideshare vehicle is in a ditch off I-70, and that passenger is dazed and hurt. A winter storm in Denver escalates quickly—both the weather and the legal aftermath. What follows is a complex insurance maze involving liability questions, medical documentation, and competing claims. Colorado law provides a three-year window to pursue compensation under C.R.S. § 13-80-101, but timing matters significantly. Under modified comparative negligence rules, C.R.S. § 13-21-111, a passenger can recover damages even if the rideshare driver is partially at fault—as long as fault doesn't exceed 50 percent. Non-economic damages, including pain and suffering, are capped at $1,500,000 as of 2025. Understanding these statutory limits and deadlines is essential for protecting passenger rights after a wreck.

This isn't a normal car accident. The key to your entire case—the only thing that truly matters—is your driver's status in the app at the exact moment of impact. That status is the switch that flips on a $1,000,000 commercial insurance policy. Under Colorado law, proving that switch was activated becomes critical to unlocking the coverage you deserve, especially given the state's modified comparative negligence standard under C.R.S. § 13-21-111, which allows recovery as long as fault doesn't exceed 50%. The insurance company will deploy predictable, cynical attempts to either deny the commercial policy applied or argue comparative negligence bars recovery entirely. Non-economic damages are capped at $1,500,000 as of 2025, making every dollar of available coverage essential. With Colorado's three-year statute of limitations under C.R.S. § 13-80-101 ticking away, aggressive legal action to establish driver status and dismantle insurance company arguments becomes not just advisable—it becomes urgent and necessary.

The Trick Insurance Companies Don’t Want You to Know

After a rideshare crash in a Denver snowstorm, the real fight isn't about what happened on the slick road—it's about what was happening on the driver's phone. Insurance companies know this distinction matters legally. Under Colorado's modified comparative negligence standard (C.R.S. § 13-21-111), a victim can recover damages even if partially at fault, as long as they're not more than 50% responsible. However, insurers will aggressively argue shared fault to minimize payouts. Evidence of driver distraction—text messages, app notifications, navigation adjustments—becomes critical in overcoming their defense. Additionally, victims must act within Colorado's 3-year statute of limitations to file suit. Non-economic damages, including pain and suffering, are capped at $1,500,000 as of 2025. Understanding these legal frameworks helps injured parties recognize when insurance settlement offers undervalue their claims and when pursuing litigation becomes necessary.

Everything—and I mean everything—hinges on which insurance policy applies. Colorado law (C.R.S. § 40-10.1-602) creates a three-tiered system that fundamentally determines compensation eligibility. A driver's status controls access to either a modest personal policy or the full $1,000,000 commercial liability policy. This distinction matters enormously because it directly impacts claim value and recovery potential. Beyond policy selection, Colorado's modified comparative negligence rule (C.R.S. § 13-21-111) allows recovery only if the injured party is less than 50% at fault—meaning shared blame can eliminate claims entirely. Additionally, non-economic damages are capped at $1,500,000 as of 2025, limiting pain and suffering awards regardless of severity. Claimants also face a critical three-year statute of limitations (C.R.S. § 13-80-101) to file suit. Understanding these interlocking rules—policy tiers, fault thresholds, damage caps, and filing deadlines—is essential. Insurance companies rely on policyholder confusion about these mechanisms to minimize payouts.

Guess which one Uber’s/Lyft’s insurers would rather not pay out?

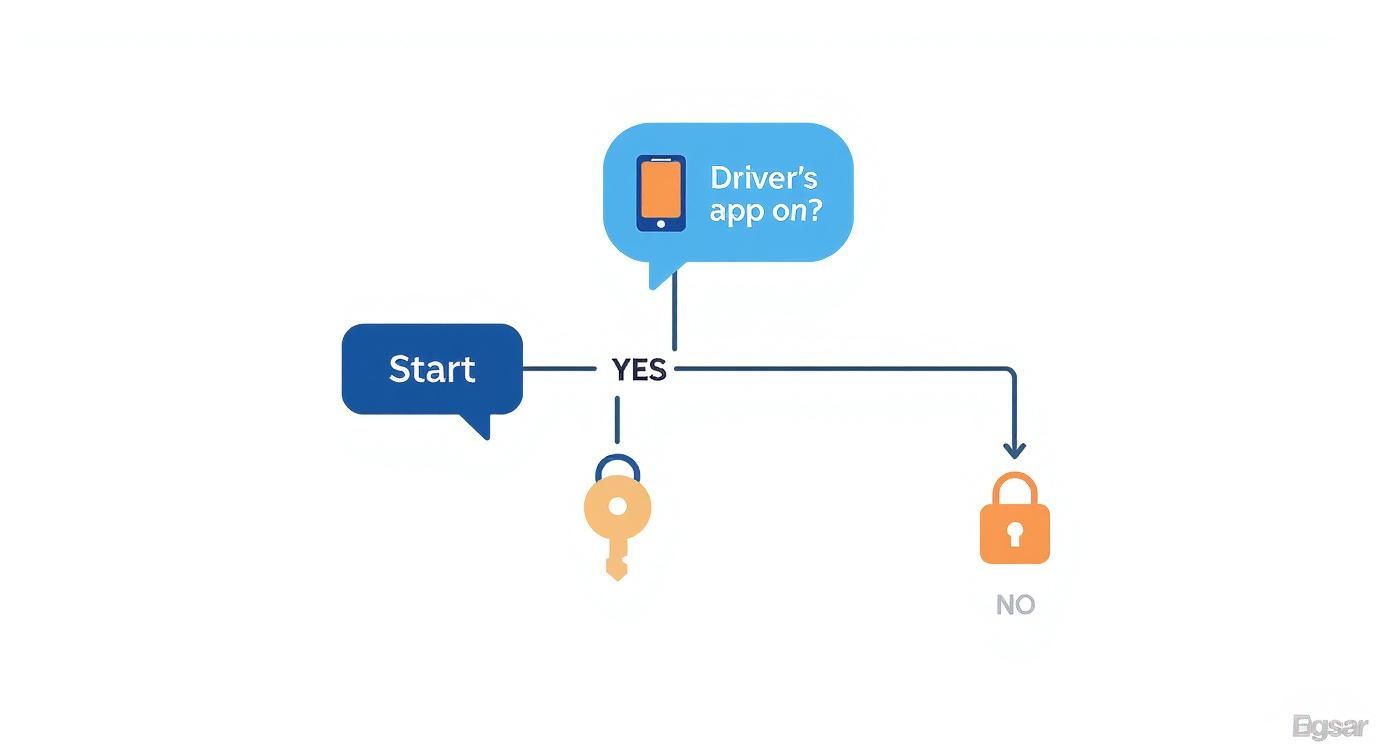

The Colorado Insurance Triad: Status is Everything

Their entire strategy is to push claims down the insurance ladder to a lower, cheaper tier. Adjusters will exploit any ambiguity or gap in documentation to save themselves a fortune at the claimant's expense. Understanding Colorado's legal framework is critical—the state imposes a three-year statute of limitations under C.R.S. § 13-80-101, meaning delayed action can forfeit valid claims entirely. Additionally, Colorado's modified comparative negligence rule under C.R.S. § 13-21-111 bars recovery if a claimant is found more than 50% at fault, giving insurers leverage to inflate negligence percentages. Non-economic damages are capped at $1,500,000 as of 2025, further limiting recovery potential. Insurance companies know these rules intimately and weaponize them during negotiation. Every vague statement, every missing medical record, every delayed response becomes justification for tier reduction. The ladder system rewards thoroughness and punishes hesitation, making early intervention and complete documentation essential to protecting claim value.

- Tier 1 (App Off): The driver’s personal policy applies. This will almost certainly be denied because of a “commercial use exclusion.” It’s a dead end.

- Tier 2 (App On, Waiting for a Ride): Limited liability coverage kicks in—typically a paltry $50,000 per person/$100,000 per accident.

- Tier 3 (Ride Accepted or In Progress): The Full Commercial Policy. This is the $1,000,000 liability coverage you are entitled to as a passenger.

This is why their first move is to try to push the claim down to the driver's smaller personal policy. It's a purely financial decision. Insurance companies understand the hierarchical structure of coverage and will exhaust lower limits before accessing commercial or umbrella policies. By settling within a personal auto policy—typically ranging from $25,000 to $100,000—they minimize their own exposure and avoid triggering higher-limit policies that could expose them to significantly greater liability. Colorado law provides injured parties with a three-year statute of limitations to file a claim under C.R.S. § 13-80-101, but early settlement pressure often exploits injured victims' desperation and medical debt. Additionally, under Colorado's modified comparative negligence standard at C.R.S. § 13-21-111, claimants cannot recover if found more than 50% at fault. With non-economic damages capped at $1,500,000 as of 2025, insurers calculate that containment strategies early in the process directly protect their bottom line.

The single most important action a passenger can take after a rideshare crash—once they are safe—is to take a screenshot of the active ride in the Uber or Lyft app. That screenshot is digital gold. It is time-stamped, geo-located proof of ride status, establishing whether the driver was operating a Tier 3 vehicle at the moment of impact. This documentation is crucial because rideshare insurance coverage hinges entirely on ride status under Colorado law. With this screenshot, the injured party provides their attorney with foundational evidence that determines which insurance policies apply. Colorado's modified comparative negligence system allows recovery even if a passenger is partially at fault, provided their negligence does not exceed 50% (C.R.S. § 13-21-111). Additionally, non-economic damages are capped at $1,500,000 as of 2025. Given Colorado's three-year statute of limitations for personal injury claims (C.R.S. § 13-80-101), preserving this early evidence immediately after a crash becomes indispensable for building a strong case.

How We Prove Black Ice Negligence in a Winter Storm

Insurance adjusters love a good snowstorm. They'll call it an "Act of God"—a convenient, almost biblical way to suggest no one is to blame. But Colorado law tells a different story. Under the state's modified comparative negligence rule (C.R.S. § 13-21-111), a property owner or business can still be held liable for winter conditions if they failed to exercise reasonable care. That might mean neglecting to salt a parking lot, failing to warn of black ice, or ignoring hazardous conditions they knew about. The injured party has three years from the accident date to file suit under Colorado's statute of limitations (C.R.S. § 13-80-101). If successful, victims may recover both economic losses and non-economic damages—capped at $1,500,000 as of 2025—for pain, suffering, and emotional distress. An "Act of God" defense only applies when conditions were truly unforeseeable and unavoidable. When negligence played a role, that defense crumbles.

Frankly, it’s nonsense. And it’s not the law.

A commercial driver has a heightened duty of care under Colorado law. These are professionals, and the legal system expects significantly more from them than from the average commuter simply trying to get home. Driving too fast for icy conditions on a commercial trip isn't an innocent mistake—it's clear negligence. Commercial drivers receive specialized training, operate larger vehicles, and carry passengers or cargo, creating a heightened standard of responsibility. When black ice causes an accident, courts examine whether the commercial driver adjusted speed and following distance appropriately. Under Colorado's modified comparative negligence statute (C.R.S. § 13-21-111), injured parties can recover damages even if partially at fault, provided they're not more than 50% responsible. Victims have three years from the accident date to file suit under C.R.S. § 13-80-101. Non-economic damages for pain and suffering are capped at $1,500,000 as of 2025. Establishing this heightened negligence standard is crucial when pursuing commercial driver claims.

Adverse weather conditions do not shield negligent drivers from liability. When black ice or winter storms are present, professional drivers—including commercial truckers and delivery operators—must still maintain control of their vehicles and operate at speeds appropriate for hazardous conditions. Rather than accepting weather as an excuse, experienced personal injury attorneys use the storm itself as evidence that the driver breached their duty of care. Under Colorado's Modified Comparative Negligence statute (C.R.S. § 13-21-111), plaintiffs can recover damages even if partially at fault, provided their negligence does not exceed 50%. Victims have three years from the accident date to file a claim under C.R.S. § 13-80-101. Non-economic damages for pain, suffering, and emotional distress are capped at $1,500,000 as of 2025. By demonstrating that a professional driver failed to adjust their behavior for winter conditions, attorneys can establish clear negligence despite challenging weather.

- Did they have adequate snow tires for the Front Range, or were they running on bald all-seasons?

- Were they driving too fast for the conditions, even if it was under the speed limit?

- Should they have even been on the road at all, or was accepting a high-risk fare to DIA during a blizzard a negligent choice?

My job is to dismantle the "Act of God" defense with cold, hard facts. We pull meteorological reports, subpoena vehicle maintenance logs, and analyze traffic data to prove the crash was foreseeable and preventable. The storm is merely the setting—the cause was a professional who failed to act like one. Under Colorado law, plaintiffs have three years from the date of injury to file a claim (C.R.S. § 13-80-101), making timely investigation critical. Colorado follows modified comparative negligence rules, meaning a defendant can be held liable even if partially at fault, provided they bear more than 50% responsibility (C.R.S. § 13-21-111). This framework allows victims to recover damages even when winter conditions played a contributing role. Non-economic damages, including pain and suffering, are capped at $1,500,000 as of 2025. These legal standards create pathways for holding negligent drivers accountable when weather becomes an excuse rather than a legitimate defense for reckless behavior.

Who Pays For Your Injuries? It’s Simpler Than They Want You to Believe.

Let's get one thing straight, because it's the only part of this mess that's simple—as the passenger, responsibility for the accident almost never falls on your shoulders. Colorado law protects passengers through a straightforward principle: the driver and vehicle owner carry liability for injuries sustained during the ride. This means coverage is nearly always available, making the passenger's position remarkably clear-cut. The real question isn't whether compensation exists—it's which insurance policy will ultimately pay. Under Colorado's modified comparative negligence standard (C.R.S. § 13-21-111), passengers can only lose eligibility if found more than 50% at fault, an exceptionally high bar that rarely applies. Additionally, Colorado law provides non-economic damage protections capped at $1,500,000 as of 2025, ensuring meaningful recovery for pain and suffering. It's crucial to remember that a three-year statute of limitations (C.R.S. § 13-80-101) applies to filing claims, so prompt action matters.

My job is to see their cynical playbook coming and cut it off at the pass.

Scenario A: Your Rideshare Driver Is at Fault

If the rideshare driver caused the wreck—whether they lost control on ice, sped excessively, or made another negligent driving decision—the liability path is straightforward. In these cases, the claim goes directly against the rideshare company's commercial liability insurance policy, which typically carries $1,000,000 in coverage. Colorado's modified comparative negligence rule under C.R.S. § 13-21-111 allows recovery even if the injured party shares some fault, provided they are not more than 50% responsible for the accident. This legal framework protects passengers from losing their entire claim due to minor contributory factors. Non-economic damages, including pain and suffering, are capped at $1,500,000 as of 2025. It's important to note that claims must be filed within Colorado's three-year statute of limitations under C.R.S. § 13-80-101. Acting promptly ensures preservation of evidence and witness testimony while protecting legal rights.

This is exactly why that massive policy exists: to protect innocent passengers and other drivers from their drivers’ mistakes.

Of course, their insurer will fight it. But with proof of active ride status and solid evidence of driver negligence, the rideshare company and its carriers can be forced to the negotiating table. Insurers don't yield to polite requests—they respond to documented claims backed by legal authority. Under Colorado law (C.R.S. § 13-21-111), modified comparative negligence rules apply, meaning a passenger can recover damages even if partially at fault, provided fault doesn't exceed 50%. Additionally, Colorado's three-year statute of limitations (C.R.S. § 13-80-101) provides a reasonable window to pursue claims without rushing settlement. Non-economic damages—covering pain, suffering, and emotional distress—are capped at $1,500,000 as of 2025, establishing a predictable ceiling for claim value. When negligence is clear and documentation is strong, insurers recognize the exposure and move toward serious settlement discussions rather than prolonged litigation. The key is presenting an airtight case they cannot dismiss.

Scenario B: Another Driver Is at Fault

What if a third party is to blame? Say, another driver slides through a red light and T-bones a Lyft vehicle. In this scenario, the primary target becomes that driver's insurance policy. Colorado law allows injured passengers three years from the date of the accident to file a personal injury claim, as established under C.R.S. § 13-80-101. However, Colorado follows a modified comparative negligence standard under C.R.S. § 13-21-111, meaning an injured party can only recover damages if they are found less than 50% at fault. If liability is clear—such as when a driver violates traffic laws—recovering compensation becomes more straightforward. Non-economic damages, including pain and suffering, are capped at $1,500,000 as of 2025. The at-fault driver's insurance carrier typically covers medical expenses, lost wages, and other documented losses, making their policy the critical avenue for recovery in third-party accident cases.

But what if they only have Colorado’s minimum $25,000 policy, or worse, no insurance at all? We pivot.

We immediately turn back to the rideshare company and file a claim against their substantial Uninsured/Underinsured Motorist (UM/UIM) coverage. This is a critical layer of protection built into their commercial policy for this exact situation. It covers injuries when the driver who caused the accident lacks sufficient insurance. Under Colorado law, rideshare companies maintain robust UM/UIM limits specifically designed to protect passengers in these scenarios. The claim process is straightforward: the rideshare company's insurer evaluates the injury damages and liability evidence. Colorado's modified comparative negligence rule (C.R.S. § 13-21-111) allows recovery even if the injured party is partially at fault, as long as fault doesn't exceed 50 percent. Additionally, non-economic damages such as pain and suffering are capped at $1,500,000 as of 2025. Importantly, injured parties have three years from the accident date to pursue a claim under Colorado's statute of limitations (C.R.S. § 13-80-101), providing adequate time to investigate and build a strong case.

When another driver causes a rideshare accident, Colorado law provides multiple layers of protection. The at-fault driver's insurance, the rideshare company's coverage, and uninsured motorist protections all work together to safeguard victims. Under Colorado's modified comparative negligence rule (C.R.S. § 13-21-111), injured passengers can recover damages even if they're partially at fault—as long as they're less than 50% responsible. This flexibility significantly expands claim possibilities. Additionally, Colorado allows three years from the accident date to file a personal injury lawsuit (C.R.S. § 13-80-101), providing ample time to build a strong case. Non-economic damages, including pain and suffering, are capped at $1,500,000 as of 2025. Understanding these protections and navigating the insurance maze requires legal expertise. A skilled attorney cuts through complexity to ensure victims access every available avenue for compensation.

Your First Moves to Secure Your Claim

The first few minutes after a crash are a blur, but quick, decisive actions can significantly impact both safety and legal claims. The immediate priority is always safety—call 911 right away to get police and paramedics on the scene. This official documentation becomes critical because Colorado law allows three years from the date of injury to file a personal injury lawsuit under C.R.S. § 13-80-101. However, evidence degrades and memories fade, making those initial moments vital for preserving crucial details. It's also important to understand that Colorado follows a modified comparative negligence standard under C.R.S. § 13-21-111, meaning an injured party can recover damages only if they are less than 50% at fault for the accident. Additionally, non-economic damages such as pain and suffering are currently capped at $1,500,000 as of 2025. These early steps—calling emergency services, documenting the scene, and gathering witness information—establish the foundation for a stronger claim while the details remain fresh and accurate.

Then, become your own best advocate.

- Screenshot Your Active Ride. I can’t say it enough. Open the Uber/Lyft app and grab a screenshot showing the active trip. This is your golden ticket.

- Call the Police. An official police report is non-negotiable. It creates an official record of the event.

- Seek Medical Attention. Go to an ER or urgent care, even if you feel fine. Adrenaline masks injuries. A medical record from the day of the crash is undeniable proof.

Now for the most important warning in securing a rideshare claim: DO NOT give a recorded statement to any insurance adjuster—not Uber's, not Lyft's, not the other driver's, and not their representatives. Recorded statements can be used against claimants later, especially under Colorado's modified comparative negligence rule (C.R.S. § 13-21-111), which bars recovery if the injured party is found 50% or more at fault. Insurance adjusters are trained to extract statements that minimize their company's liability. Any admission, clarification, or seemingly innocent remark can be weaponized to argue contributory negligence. Colorado law allows three years from the injury date to file a personal injury lawsuit (C.R.S. § 13-80-101), but early statements made during the investigation phase often cause irreparable damage to otherwise viable claims worth substantial compensation—including non-economic damages capped at $1,500,000 as of 2025. Protect the claim by declining all recorded statements and referring all inquiries to legal counsel.

Their first move is always to try to push the claim down to the driver's smaller personal policy limits. That's why these calls are not designed to help—they are carefully planned interrogations meant to trap the injured party. Insurance adjusters use recorded statements to lock claimants into disadvantageous narratives before they fully understand the extent of their injuries or legal rights. Under Colorado's modified comparative negligence standard (C.R.S. § 13-21-111), a claimant can recover damages even if partially at fault, provided negligence doesn't exceed 50%. However, early statements can be weaponized to establish comparative fault. Additionally, Colorado law provides a three-year statute of limitations to file suit (C.R.S. § 13-80-101), but waiting too long weakens negotiating power. Non-economic damages, including pain and suffering, are capped at $1,500,000 as of 2025. Understanding these legal frameworks before speaking with insurers protects claimants from inadvertently reducing their recovery potential.

Politely decline and tell them your attorney will be in touch. That's it. End the conversation. Understanding the complex world of navigating insurance claims and disputes requires legal expertise—that's precisely why having an attorney handle these communications matters. Insurance adjusters are trained negotiators, and anything said can be used to minimize claim value. Colorado law recognizes this dynamic. Under C.R.S. § 13-80-101, injured parties have three years from the date of injury to file a personal injury lawsuit, but early communication with legal counsel protects rights throughout the claims process. Additionally, Colorado's modified comparative negligence rule under C.R.S. § 13-21-111 allows recovery only if the injured party is 50% or less at fault. Non-economic damages are capped at $1,500,000 as of 2025. These legal nuances demand professional guidance. For a more complete checklist on protecting a claim from its earliest stages, consult a detailed guide on what to do after a car accident or personal injury incident.

Disclaimer: The information provided in this article is for general informational purposes only and does not constitute legal advice. The content is not intended to create, and receipt of it does not constitute, an attorney-client relationship. You should not act or refrain from acting based on this information without seeking professional legal counsel. The outcome of any legal matter depends on a variety of factors, including the specific factual and legal circumstances, and past results do not guarantee a similar outcome in future cases. Conduit Law is a law firm licensed to practice in Colorado.

You’ve been through enough. Let me handle the insurance fight so you can focus on getting better. I’ve got you.

Written by

Conduit Law

Personal injury attorney at Conduit Law, dedicated to helping Colorado accident victims get the compensation they deserve.

Learn more about our team